The Complete Gap Insurance Guide

Here's Everything You'll Ever Need To Know About Gap Insurance...

Considering Gap Insurance But Still A Little Unsure? Maybe You Just Need A Few Things Cleared Up? Don’t Worry, Our Complete Gap Insurance Guide Has Got You Covered…

If you’re currently in the market for a new car (whether that’s brand spanking new, or new to you), the chances are you’ve probably come across the terms; ‘depreciation’, ‘negative equity’ and ‘gap insurance’, but what exactly do they all mean? And why are they so important?

In this guide, we’re looking at all things Gap (Guaranteed Asset Protection), why it should matter to car owners and whether it’s right for you. Before focusing on Gap Insurance, let’s understand the basics of depreciation and negative equity.

Quick Links

- What Is Gap Insurance?

- What Are The Different Types Of Gap Insurance?

- Choosing The Right Type Of Gap Insurance

Car Depreciation

Over time your car will lose value, usually due to factors such as added mileage, wear and tear, desirability (particularly when newer models are released), engine type (for instance, diesels, now out of favour, are suffering greater losses in value) and general ageing. This loss in value is referred to as ‘Depreciation’.

Depreciation is usually given as a percentage of the original value of your car. For example, a £30000 car losing £3000 of its value would have suffered a 10% depreciation.

In all but rare cases (such as during COVID, when demand for cars outweighed supply) depreciation is inevitable and should be factored into the cost of your motoring, in short; your car is a depreciating asset.

We’ve covered car depreciation in greater detail in our article: Why Do Cars Depreciate?

Negative Equity

Here is where car depreciation gets troublesome. When your car depreciates at a faster rate than your finance repayments cover (such as PCP or HP repayments) then you could be in negative equity; meaning your car is worth less than the amount outstanding (that you owe) on finance.

Example: A new Tesla Model Y retails for £52000, however, due to depreciation (of 19.9%), after one year of ownership its resale value is approximately £42000, a ‘loss’ of £10000.

At the same time, monthly repayments on the car might be £500 per month, meaning that in the same year, you’ll have repaid £6000, leaving a balance on the car of £46000.

The result? You have a car worth £42000 that you still owe £46000 on! That’s a negative equity amount of £4000 (the difference between the amount you owe and the car value). Worse still, this is a ‘best case scenario’ example, which doesn’t include interest on finance repayments.

Interested in learning more about EVs? Read our guide: How Much Do Electric Vehicles Depreciate?

This negative equity can cause issues if your car is declared a ‘total loss’, which is where Gap Insurance becomes useful. Let’s look at Gap in more detail:

What Is Gap Insurance?

In simple terms, Gap Insurance makes up the difference between the amount your car is worth and the amount you paid; if it’s ever declared a ‘total loss’ or ‘write-off’.

When your car is written off, your insurance company will usually pay the amount your car is worth at the time, not the amount you paid. As we’ve discovered, this can be much less, thanks to depreciation. With Gap Insurance you have less worry, as the difference is covered in your policy.

Gap Insurance Meaning

Gap stands for ‘Guaranteed Asset Protection’, also known as Shortfall Insurance, Invoice Gap and Purchase Protection. Some people may also refer to specific types of Gap Insurance under the same name, such as RTI Insurance, PCP Gap and Lease Gap (we’ll explore these below).

What Are The Different Types Of Gap Insurance?

Lease & Contract Hire Gap Insurance

Leasing (or Personal Contract Hire) is a popular choice for new cars, with 1.6 million people choosing it in the UK each year. It’s an attractive option as motorists can drive a brand-new car (without full ownership) at a moderate monthly repayment level.

However, if the lease car is involved in an accident, stolen or damaged beyond repair and written off, sadly, you’ll still be liable for repayments. This can be particularly problematic on lease vehicles as most cars depreciate at their quickest rate in the first 1-3 years, meaning a potentially bigger shortfall.

Lease & Contract Hire Gap Insurance, also known as Lease Gap or PCH Gap, pays the difference between your car insurance settlement and the amount outstanding on the finance/lease, reducing your risk of financial liability.

Return To Invoice Insurance

Return To Invoice Insurance, or RTI Insurance as it’s often known, is the most popular type of Gap Insurance available on the market; particularly with cars financed through PCP or HP.

Similarly to Lease Gap Insurance, RTI pays the difference between your car insurance settlement figure and the invoice price of your vehicle so you won't be affected by any depreciation or negative equity your car may have accumulated.

Return To Invoice Insurance is available on new and used cars, provided you bought your car recently (usually within 180 days).

Other Types Of Gap Insurance

Depending on your circumstances, the type of vehicle you are buying and how you are financing the purchase you may be interested in other types of Gap Insurance such as:

- Agreed Value Insurance: Agreed Value policies pay the difference between your motor insurer’s settlement figure and the agreed retail price of your car at the time of your policy purchase; effectively, negating depreciation.

- Vehicle Replacement Cover: This cover pays the difference between your settlement figure and the amount needed to replace the vehicle (like for like). Vehicle Replacement Cover can be particularly useful as it removes the hassle of ‘haggling’ with insurers over the money needed to get a similar car and get back on the road.

Usage Data For Gap Insurance

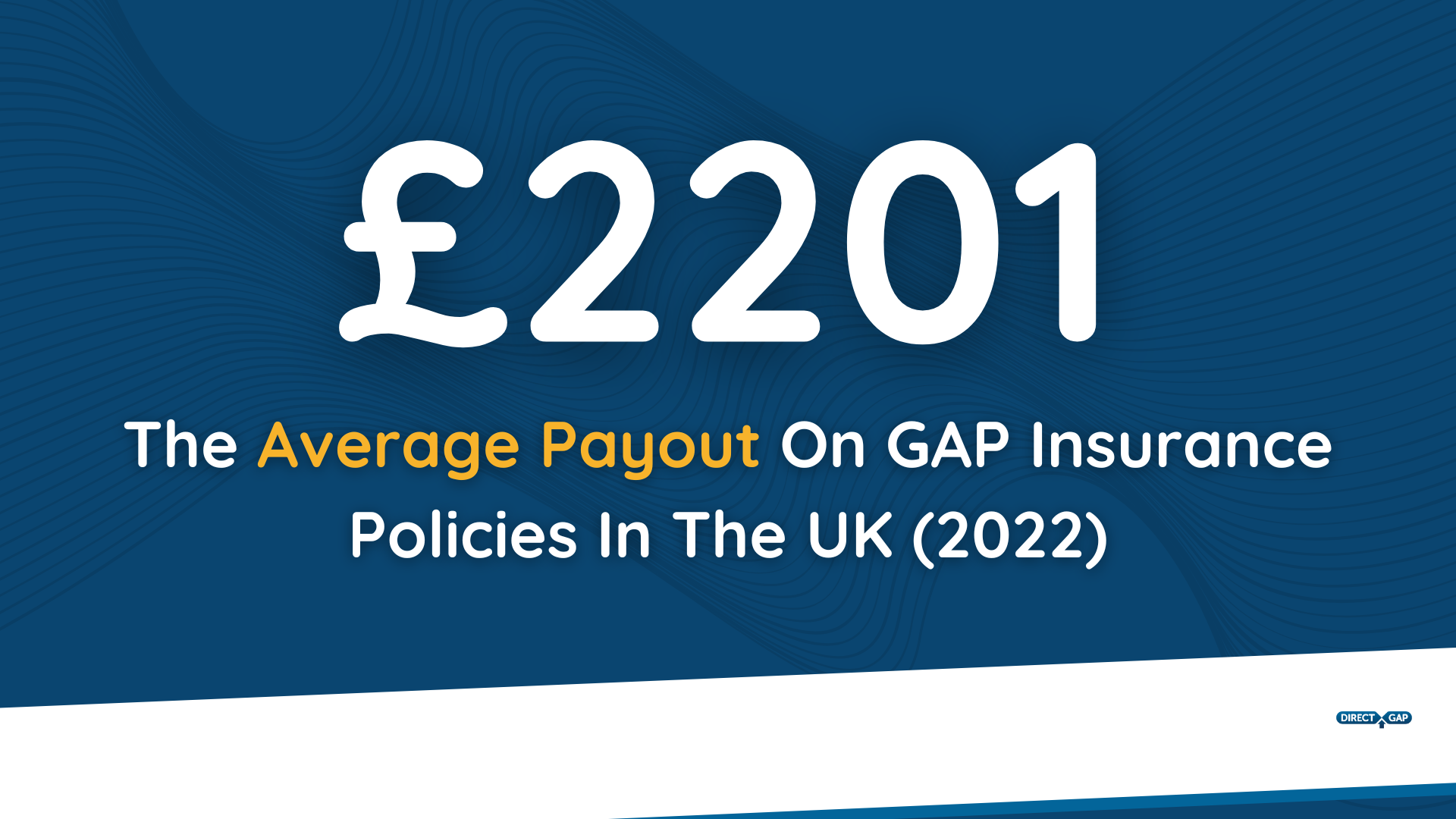

According to FCA data there were 2.4 million Gap Insurance policies in force in the UK in 2022.

The average payout on Gap Insurance policies throughout the UK was £2201 with a 99.3% payout rate on standalone policies.

Choosing The Right Gap Insurance

Frequently Asked Questions About Gap Insurance

Is Gap Insurance Worth It?

Whether Gap Insurance is ‘worth it’ depends entirely on your circumstances and whether you think there is value in protecting yourself against financial shortfall. It’s worth remembering that you could be financially liable for the negativity equity in your car (something almost inevitable) if the worst happens.

Factors to consider include how much depreciation your car may experience (for instance, new cars tend to depreciate at a higher rate than older cars), your financial situation and your degree of financing.

As we’ve already discussed, the average payout rate for Gap Insurance industry-wide is 99.3%, with an average payout value of £2201, meaning most drivers avoid a shortfall of over £2000 just by using their policy.

How Does Gap Insurance Work?

Following a total loss; Gap insurance pays the difference between your car insurance settlement and the amount outstanding on your car, or the amount you paid for it, depending on the policy you choose.

How Does Gap Insurance Work On A Financed Car?

It depends on the type of finance you have. For instance, Lease Hire Gap Insurance will return your finance balance to zero. Return To Invoice Insurance will cover the difference between your vehicle value and the invoice figure.

What Does Gap Insurance Cover?

Gap Insurance effectively covers the negative equity your car may have accrued. Following an accident, fire or theft, where your car is declared a total loss, Gap Insurance will cover the difference between how much your insurer is willing to pay out and the amount you paid, or still owe, which is often much more, thanks to depreciation and negative equity.

Our policies cover all named drivers on your regular motor insurance.

Can I Get Gap Insurance On A New Car?

Yes, Lease Gap Insurance, Return To Invoice Insurance, Agreed Value Insurance and Vehicle Replacement Cover are all available for new cars. However, suitability varies, usually depending on the way your purchase is financed.

For example, Lease Gap Insurance isn’t suitable for new cars purchased on PCP and vice versa.

Can I Get Gap Insurance On A Used Car?

Some Gap Insurance products are available for used cars, such as RTI Insurance and Vehicle Replacement Cover. There are often limits on policies such as the age and mileage of the car.

Which Gap Insurance Is Best For Cars On Lease?

There are several policies available for lease cars, however, we provide a dedicated Lease Hire Gap Insurance.

Which Gap Insurance Is Best For Cars On PCP?

There’s no ‘best’ policy for cars financed via PCP. However, most of our customer choose Return To Invoice Insurance to cover their PCP car.

Buying or driving a car on PCP? Read our guide: Common PCP Mistakes (That Could Cost You Money)

When Can I Buy Gap Insurance?

You can buy Gap Insurance online up to 180 days after purchasing your car (this timeframe may change and vary by provider). If you’re considering buying Gap Insurance through a dealership, by law, you should only be able to buy it 48 hours after buying your car; not at the same time.

This allows some ‘thinking time’ to explore other options before committing, helping you avoid buying an expensive policy in the heat of the moment.

Should I Buy Gap Insurance Online Or From A Dealership?

Whether you buy Gap Insurance online or from a dealership is a personal preference. However, there are a few things to understand if you opt for a policy via a dealership:

- Outsourced Policies: Dealership Gap Insurance policies are often branded as their product when in reality, they are provided by a third party. This means you will deal with an external provider if you need help, or to make a claim.

What’s more, you could also be paying a premium, which the dealership includes as their margin. - Pay Monthly Policies: One of the main selling points of a dealership policy is the ability to include your Gap Insurance in the overall purchase of your car and pay monthly. However, pay monthly gap insurance is widely available online and through other dealers.

- Price: Dealership Gap Insurance is almost always more expensive than buying a policy online. In most cases, this is down to dealership profit margins which are much higher than buying online; without any difference in coverage.

Read More: Why Buy Gap Insurance Online Instead Of From Dealers

Can You Purchase Gap Insurance On Your Own (Not Through A Dealership)

Yes! You can purchase Gap Insurance, Return To Invoice Insurance and Vehicle Replacement Cover online.

Does Gap Insurance Still Exist?

Gap Insurance is still available online and from select dealerships using regulated underwriters.

In recent years the FCA (Financial Conduct Authority) reduced the number of providers, following action to improve fair value. Direct Gap is one of the remaining providers regulated by the Financial Conduct Authority.

In 2015, the FCA also introduced a 48-hour ‘grace’ period for buying Gap Insurance from a dealership, allowing buyers to explore other options before committing. In many instances, dealerships chose not to ‘push’ or offer Gap after this, which is why it may seem less prevalent when buying a car these days.

Is Gap Insurance Regulated?

Gap Insurance is regulated by the Financial Conduct Authority. They ensure selling of Gap Insurance is transparent and fair.

Our Final Word

As you’ve probably discovered, there’s more to Gap Insurance than most people first realise. That said, we know it can sometimes be confusing, we hope this article has cleared things up for you; if there’s anything you’re still unsure about get in touch!

We’re always happy to help; the more you know about Gap, the better for us! Call us, or contact Luke on social media. Don’t forget to drop us a follow on Facebook for more helpful content where we cover all things car-related.

Pin It!

Luke Sanderson

Luke is our resident copywriter, combining plenty of automotive experience, particularly in car sales with a commitment to well-researched, extensive writing. He draws on his own experiences, as well as quizzing the entire team at Direct Gap to ensure the blogs and articles you read are worthwhile, valuable and accurate. Got a question for Luke? Drop us a DM on social media and he'll be happy to help.